Digital health funding surges to $7.4B in Q1 2026, but mega-rounds dominate investment landscape

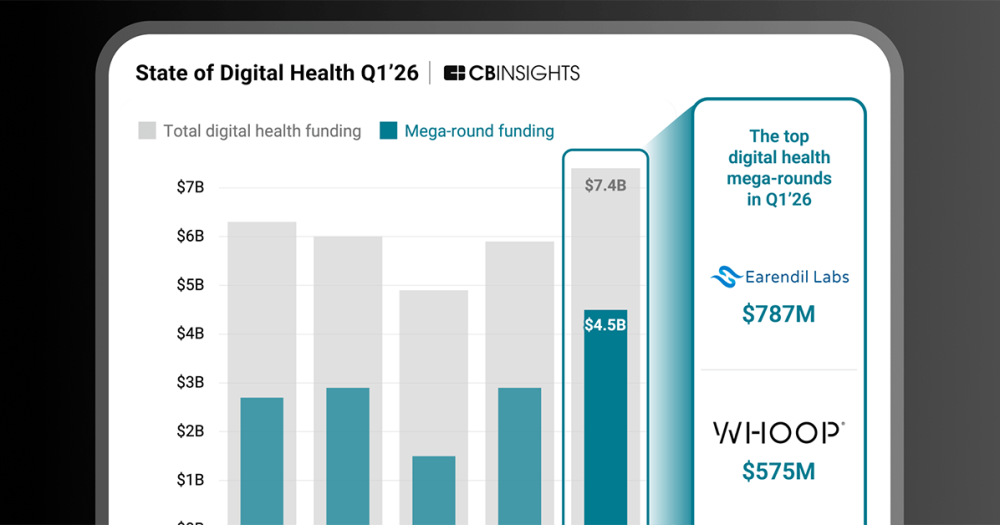

Digital health opened 2026 with strong momentum, but the sector has become increasingly top-heavy. Funding rose to $7.4B in Q1 2026, up from $5.9B in Q4 2025 and reaching its highest level since Q2 2022.

However, the money concentrated around a narrow set of category leaders. Mega-rounds of $100M or more accounted for 60% of all funding across just 19 deals — the highest share in recent quarters. Average deal size climbed to $29.6M, up 46% year-over-year, as investors made fewer but bigger bets.

Highlights

- Digital health funding hit $7.4B in Q1 2026, the highest since Q2 2022

- 19 mega-rounds captured 60% of all capital raised

- Eight new unicorns emerged — the most since Q2 2022

- M&A deal count jumped 47% to 56 transactions

- CMS prior authorization deadline driving investment activity

- Pharma committed billions to AI drug discovery platforms

- Healthcare AI hiring surged as competition broadens

Why does it matter?

This data reveals a digital health sector reorganizing around proven winners. The concentration of capital in mega-rounds shows investors have become more selective, focusing on companies with demonstrated scale and commercial success rather than early-stage potential.

The trend has major implications for the industry. Well-funded unicorns like Devoted Health and Alan can now stay private longer, build distribution, and acquire competitors rather than be acquired. This creates a two-tier market where the top companies pull further ahead while smaller players struggle for funding.

The CMS prior authorization mandate, requiring fully electronic systems by January 2027, is also creating urgent investment opportunities. Companies that solve this regulatory requirement face a clear market deadline, making them attractive targets for both investors and acquirers.

The context

Digital health has been recovering from the funding crash of 2022-2023, when investor enthusiasm cooled after pandemic-era highs. The Q1 2026 results suggest the sector has found its footing, but only for companies that can prove real-world adoption and revenue growth.

The M&A activity tells this story clearly. Abbott's $23B acquisition of Exact Sciences wasn't just about regulatory approval — Exact's Cologuard had already completed 20 million screenings with Medicare coverage. Meanwhile, companies with regulatory clearance but minimal revenue struggled to command premium valuations.

In AI drug discovery, the split between large pharma deals and early-stage funding reflects different strategies. Established players like Earendil Labs ($787M raise) and partnerships with Takeda (up to $1.7B committed) focus on compressing existing R&D timelines. Early-stage companies are betting on entirely new drug classes and modalities.

The hiring surge in healthcare AI, led by companies like Tennr and Hippocratic AI, signals the market moving from product development into enterprise deployment. Even tech giants like Anthropic and Nvidia are expanding healthcare-focused roles, suggesting 2026 will see increased competition for healthcare AI talent and market share.

Latest @

What a pregnant woman eats can shape her child's health for life, new research shows

Dubai hospital becomes first in the Gulf to use advanced 3-in-1 heart artery imaging system

Abu Dhabi researchers find new clue in the fight against Huntington's disease

M42's national lab partners with Abbott to bring early cancer detection to the UAE

💡Did you know?

You can take your DHArab experience to the next level with our Premium Membership.👉 Click here to learn more

🛠️Featured tool

Easy-Peasy

Easy-Peasy

An all-in-one AI tool offering the ability to build no-code AI Bots, create articles & social media posts, convert text into natural speech in 40+ languages, create and edit images, generate videos, and more.

👉 Click here to learn more